The year 2025 has ushered in a period of significant economic and geopolitical instability, challenging long-held beliefs about global financial stability. Traditional safe havens, once considered secure pillars of investor confidence, are now being reevaluated considering shifting dynamics. The United States, historically seen as the backbone of global markets, finds itself in the middle of growing uncertainty, prompting investors to seek refuge elsewhere. This article explores the evolving landscape of currency movements, asset preferences, and the broader consequences brought on by a weakening US dollar.

At the heart of this transformation lies a variety of factors: political unpredictability, fiscal strain, and a recalibration of monetary policy. The Trump administration’s return to the White House has introduced fresh volatility, with trade tensions and ballooning deficits casting doubt on America’s financial trajectory. As a result, investors are increasingly turning to alternative stores of value such as gold, hard assets, and resilient currencies like the Swiss Franc and Japanese Yen. These shifts are not only reactive but signal a deeper rethinking of risk and return in a world where the dollar may no longer reign supreme.

This reassessment has had a major impact across emerging markets, especially in South Africa, where the rand has demonstrated unexpected resilience. However, this strength is less a reflection of domestic robustness and more a symptom of the dollar’s decline. The global currency landscape is undergoing a subtle but significant transformation, with the Euro and Pound gaining ground and the dollar losing its grip. The implications of this trend extend beyond exchange rates, influencing the direction of capital flows, investment strategies, and the future of the global trade landscape.

As we delve into the analysis presented by Izak Odendaal and other market commentators, it becomes clear that 2025 marks a turning point. The dollar’s retreat is not a collapse but a gradual unwinding of a 15-year ascent, shaped by structural shifts and investor sentiment. This article offers a timely examination of these developments, providing insight into how markets are adapting and what the future may hold for global investors in an era of uncertainty.

Say goodbye to the US dollar as you know it

By Shaun Jacobs • Daily Investor 16 September 2025

Amid increased volatility and uncertainty in 2025, investors have not turned to the US dollar as a historical safe haven, preferring other assets and even other currencies.

As the United States’ financial health deteriorates and the Trump administration introduces fresh volatility into markets, investors searching for safety have largely turned to gold.

Other hard assets are also seeing increased interest from investors, as well as some currencies like the Japanese Yen and Swiss Franc.

This has been a major factor in the relative appreciation of the rand versus the dollar so far in 2025, with the greenback weakening more so than the South African currency strengthening.

The strength of the euro and pound versus the rand shows that this is the case, as the dollar has broadly weakened against global currencies.

Old Mutual’s Symmetry chief investment strategist Izak Odendaal explained that investors are running to hedge the dollar.

Borrowing this phrase from the Financial Times, Odendaal said the decline in the US dollar is probably the most notable market development this year.

After the Liberation Day shock, many commentators – including Odendaal – noted that international investors would reassess their US overweights, and that this would be a drag on the dollar.

What seems to have happened instead was a rush to hedge out currency risk, rather than pulling out of US bond, equity and credit markets.

The latter two remain in rude health in particular, but the bond market is also still attracting inflows, albeit on a relatively smaller scale.

Odendaal said that after more than a decade of being FX unhedged, which was beneficial for many large international investors as the dollar strengthened, there is much catching up to do.

Ongoing hedging activity could weigh on the dollar even if United States asset returns are fine. Indeed, it can become self-fulfilling, as expectations of dollar weakness lead to increased hedging activity.

With the Fed probably about to embark on a cutting cycle, interest rate dynamics could increasingly reassert themselves, and they are also not dollar bullish.

For emerging markets, dollar weakness has been a significant boost and could continue to be in the medium term.

Despite the third-worst yearly performance for the dollar index so far in 2025, it remains pretty strong by historical standards, with room to ease further.

However, Odendaal warned that nothing happens in straight lines, with periods of relative dollar strength expected while the broader trend is weakness.

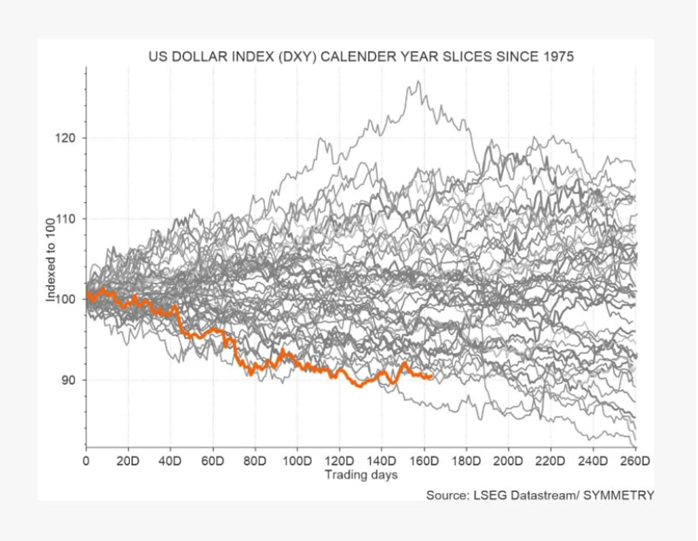

The dollar’s poor performance so far in 2025 can be seen in the graph below.

Dollar on the backfoot

The dollar’s weakening so far in 2025 indicates that its inexorable rise for the past 15 years appears to be coming to an end.

Odendaal explained that this has very little to do with the dollar potentially losing its status as the world’s reserve currency. It remains dominant in that sphere without much change over time.

Furthermore, the dollar remains the primary currency used for global financial flows, making it indispensable for global trade.

Investors are increasingly concerned about America’s financial health and whether or not the outperformance of its equity markets will continue.

This means that the rand’s steady weakening against the US dollar may be coming to an end, not necessarily because of the South African currency’s strength but because the greenback is losing ground.

So far in 2025, investors have shied away from investing in the traditional safe haven of US Treasury bonds, looking to Europe, Japan, and Switzerland for enhanced stability.

This is largely a result of the increased uncertainty created by US President Donald Trump’s imposition of tariffs on the country’s trading partners and increased scepticism of the financial health of the US government.

The United States continues to run record deficits out of wartime, increasing its debt load to over $36 trillion, and resulting in it spending more on servicing its debt than on its renowned military.

Odendaal said the dollar’s strength over the past 15 years largely reflects stronger economic growth in the United States and, consequently, higher interest rates, which attract capital.

Moreover, the stunning outperformance of its large technology shares made the United States equity market a must-own for investors worldwide.

As the dollar gained, it boosted the value of US investments for non-US investors and similarly made international investments unattractive for Americans.

In addition to geopolitical risk, such as Russia’s war in Ukraine, and at the start of the year, the real trade-weighted dollar index was shown to be near its highest level since 1970.

In 50 years, it was only stronger 5% of the time. From this elevated level, there is naturally little upside and plenty of room to decline, Odendaal said.

The catalyst for the dollar’s decline in value is President Trump’s trade and fiscal policies. Initially, the dollar rallied on his election, on the expectation that US growth outperformance would be given a boost.

However, since he took office, there has been a lot about the Trump administration that has made investors nervous.

This can be seen in the decoupling of the dollar from interest rate differentials. Normally, elevated US interest rates would have resulted in a stronger dollar. Instead, it has fallen 13% against the euro this year.

Apart from the tariff uncertainty, investors’ biggest concerns include the inexorable rise in US government debt levels and the independence of the Federal Reserve.

")

")

")

")