Managed Portfolios versus Fund of Funds

In the words of Mark Twain – “The only two certainties in life are death and taxes.” In South Africa, this is most certainly true, especially when it comes to Capital Gains Tax (CGT).

When does CGT come into effect?

CGT comes into effect with the disposal of an asset (be it a house, a unit trust, etc.). A disposal is triggered by the sale of an asset, donation thereof, upon a person’s death, should you cease to be a South African resident, or with the loss or destruction of an asset. In the world of investments, if you disinvest from an investment (wholly or partly), it is seen as a ‘sale’ of an asset and will therefore trigger CGT. This is also true when you disinvest from one fund to invest in another – depending on the type of investment vehicle you are invested in.

For example, if you are invested in a Model Portfolio and your Discretionary Fund Manager (DFM) makes changes to your portfolio (like disinvesting from cash to buy more equity holdings), you will be required to pay CGT on any capital gains realised. The opposite is true in the case of a Fund of Fund investment, where you do not pay CGT on rebalances or changes within the Fund of Fund but you will still be liable for CGT when you withdraw your investment at the end of your investment term. One thing remains certain – you will have to pay the taxman at some stage.

The question of using your CGT allowance and the effectiveness thereof in a Model Portfolio has been a question many advisers and their clients have grappled with. Is it tax-efficient to make use of your annual CGT allowance when your investments are restructured/rebalanced and managed by a DFM? Should you make use of an investment vehicle like a Fund of Fund that only requires you to pay CGT when you decide to withdraw your funds?

Good news – we’ve crunched the numbers and have come up with an answer. With that being said, we are not claiming to be tax experts. In the following article, we look at two investment vehicles and one strategy and the implications of CGT on these three approaches –

- Model Portfolios (investment vehicle)

- Fund of Funds (investment vehicle)

- A buy and hold strategy (investment strategy)

Before we go into detail, let us first look at the characteristics of each of these strategies to get a better understanding of the results.

A Model Portfolio

A Model Portfolio is a collection of unit trusts that are “wrapped” together under the instruction of a registered Discretionary Fund Manager (DFM) and is available via a Linked Investment Service Provider (LISP) platform through a financial adviser. The funds within the Model Portfolio are held by the investor directly, invested via an investment platform and managed and rebalanced by the DFM on behalf of the investor. Each of the underlying funds within the portfolio is detailed on an investor’s statement.

A Fund of Fund

A Fund of Fund, in essence, uses the same concept, with the main difference being that the funds within a Fund of Fund are not held by the investor directly. The unit trusts are pooled into a singular fund, called a “Collective Investments Scheme” (CIS) and the investor holds units in this CIS fund. On a client statement, the underlying funds will not be seen. This essentially means that, when changes are made within the fund, CGT is not triggered, as it is seen as a trading change and not a disposal of assets, which is exempt from tax.

A buy and hold strategy

Although this is not an investment vehicle (as is the case with Model Portfolios and Fund of Funds), we wanted to investigate the impact of CGT on this strategy as well. With a buy and hold investment strategy, an investor buys into a unit trust (or a share) and holds the investment for the long-term. No changes are made until such time the investor decides to disinvest from the investment. Only when the investor redeems his/her funds, will CGT be triggered.

Harvesting your annual allowance versus redeeming at the end of your investment

Now that we have a good idea of the different investment vehicles/strategies we considered; we can look at some of the assumptions used to crunch the numbers.

Our assumptions:

- The first assumption is that an investor (“investor A”) invested the following, on 1 January 2005 –

- R1 million in a Model Portfolio,

- R1 million in a Fund of Fund

- R1 million in “Investment X” and followed a buy and hold strategy.

- CGT was calculated with a 40% inclusion rate and R40 000 exclusion (at set out by SARS) and we assumed that Investor A has a marginal tax rate of 30%.

- For our Model Portfolio investment –

- We will rebalance the portfolio annually.

- Every time the portfolio is rebalanced back to its static weights, CGT will be triggered.

- For our Fund of Fund investment –

- We will also rebalance annually to static weights.

- As mentioned, for a Fund of Fund the rebalances will not trigger CGT but Investor A will have to pay CGT at the end of his investment when the investment is redeemed.

- With our buy and hold strategy –

- We will keep the portfolio as is and no rebalancing will take place, CGT will be payable (as with a Fund of Fund) at the end of the investment term when the investment is redeemed.

Investor A will be investing in a fictional balanced portfolio called “Investment X” where a building block approach is taken when constructing the portfolio. In a building block approach, a DFM takes control of the asset allocation and selects specialist managers to fill each of the building blocks within the portfolio. In other words, the DFM hand-picks the manager that is allocated to equity, property, cash, offshore and bonds etc.

In “Investment X” we have used indices as a proxy for each building block. The weightings of “Investment X” has been included below:

Let’s investigate what the numbers have to say

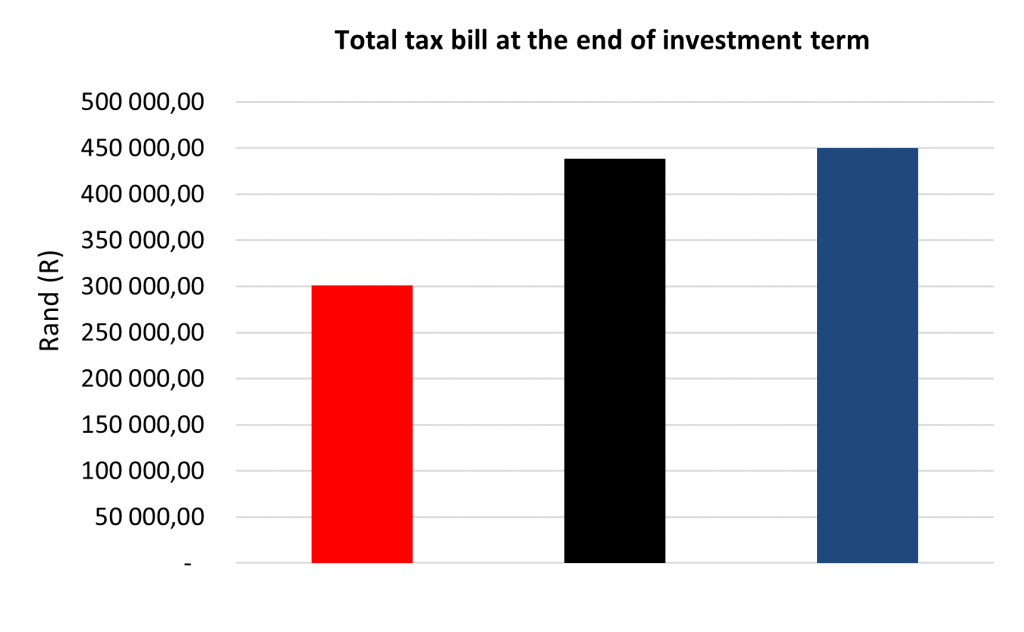

Considering the three different approaches Investor A followed, where did he/she pay the most CGT at the end of the investment period in December 2020?

As can be seen in the below graph, the Model Portfolio investment (which was rebalanced annually and made use of CGT allowance harvesting) had the smallest CGT tax bill over the period under review. This equates to a tax saving of 31% when compared to the investment in a Fund of Fund and a 33% tax saving when compared to the buy and hold strategy.

Buy and Hold Fund of Fund Model Portfolio

Source: Morningstar Investment Management. Data as at 30/11/2021. For illustrative purposes only.

Given that we had to pay CGT annually in the Model Portfolio, how would this impact the return of the investment over the period under review?

The Model Portfolio investment would generate an annualized return of approximately 9,5%. If we consider the return of the other two strategies, there is a marginal difference, with the Fund of Fund sitting at an annualized return of 10,3% over the investment period.

In conclusion

As counterintuitive as it may seem, rebalancing annually and using your annual CGT allowance is optimal, the difference in returns between the three approaches are marginal but the real difference comes through when we compare the total tax bill at the end of the investment term. When it comes to tax and ensuring your investment strategy follows the most tax-efficient approach, we recommend consulting your financial adviser or a tax professional. K

Risk Warnings

This commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar Investment Management South Africa (Pty) Ltd makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this commentary. Except as otherwise required by law, Morningstar Investment Management South Africa (Pty) Ltd shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use.

This document may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

Morningstar Investment Management South Africa Disclosure

The Morningstar Investment Management group comprises Morningstar Inc.’s registered entities worldwide, including South Africa. Morningstar Investment Management South Africa (Pty) Ltd is an authorised financial services provider (FSP 45679) regulated by the Financial Sector Conduct Authority and is the entity providing the advisory/discretionary management services.

+ t: (0)21 201 4645 + e: MIMSouthAfrica@morningstar.com + 5th Floor, 20 Vineyard Road, Claremont, 7708.

")

")

")